In this month’s issue of Signal, we dive into the new EU Clean Industrial Deal, we look into policies for decarbonising the cement industry, and we give a run-down on low-emission chemicals in Brazil.

In an ever-changing world, partnerships paving the way for a newer, cleaner industry continue, driven in part by the common understanding that a market transition is underway and by the need to keep in step with respective local policy action. This month’s Signal delves into the transition for two key sectors and the policies driving them:

The wait is over, now we need to pick up the pace to fulfil ambitions.

As revealed at the end of February, the Clean Industrial Deal (CID) lays open the European Commission’s (EC) plan to take advantage of the growth opportunities for European companies in the move to a clean industry. Europe has led on technological developments and first-of-a-kind projects but needs to move from this demonstration phase to a commercial reality. Today, Europe is home to a fifth of the pipeline of announced clean industry projects worldwide, but these projects are struggling to reach Final Investment Decision (FID), which is when they are fully confirmed and start construction, and momentum is building in other regions of the world.

Over time, the CID has the potential to have an important impact on EU industry, but the extent of its influence will be unclear until the details materialise over the next two years. Today, this much is sure: The EC needs to work quickly to turn this promising vision into material steps in the face of rapidly mounting challenges to European industrial competitiveness.

The deal’s plans to reduce European energy costs and mobilise funds likely to unlock hundreds of billions in support for clean technologies are welcome news, but in isolation, it is not enough. Much lower labour and (renewable) energy costs in other parts of the world will likely still make it challenging for the EU to be competitive in producing essential commodities like fertilisers and materials. So, what will be the trade off? Will Europe choose to protect its industrial base for sovereignty and resilience reasons at the expense of global competitiveness; or will it develop clean trade partnerships to diversify imports of the most energy-intensive parts of key industrial value chains while maintaining technology leadership and higher-value segments of industry? This doesn’t appear to have been fully thought through yet.

Low-carbon demand and breaking bottlenecks

The CID also acknowledges the significance of creating lead markets for clean commodities – breaking down one of the key barriers to clean industry. This is something we have been talking about for the past six months and the importance is hard to overstate.

Developing demand for clean commodities through policy is a critical piece of the puzzle that was missing in Europe up to this point but is now well embedded in this deal. There have been pioneering voluntary efforts to build demand for clean industry products, but policies are necessary to create the scale of demand needed to unlock project construction. However, with detailed measures yet to be seen, we would urge the EC to develop precise proposals for the use of product standards and mandates to drive clean commodity demand from the public and private sector – at scale and across all key industrial value chains. SThere are learnings to take from other sectoral policies like the ReFUEL-EU SAF mandate, which has proven to be an efficient tool to unlock investment in SAF plants, even if it has come under attack recently. If done right this type of mandates could trigger early markets for clean commodities.

Including the private sector will be particularly important as public procurement can only hit a significant scale in sectors where it is a major buyer, like cement. Promoting private procurement will be necessary where the public sector is not a sizeable purchaser, for example, for chemicals.

There are some tough decisions on the horizon to balance fostering the clean industry of the future leveraging the European domestic market and looking for new export markets too, while diversifying supply chains to source some cheaper components from abroad.

The great hope for the CID is that it focuses on unlocking the healthy pipeline of clean projects which already exist in Europe so they can start construction and go on to make a difference to European economic development and greenhouse gas emissions.

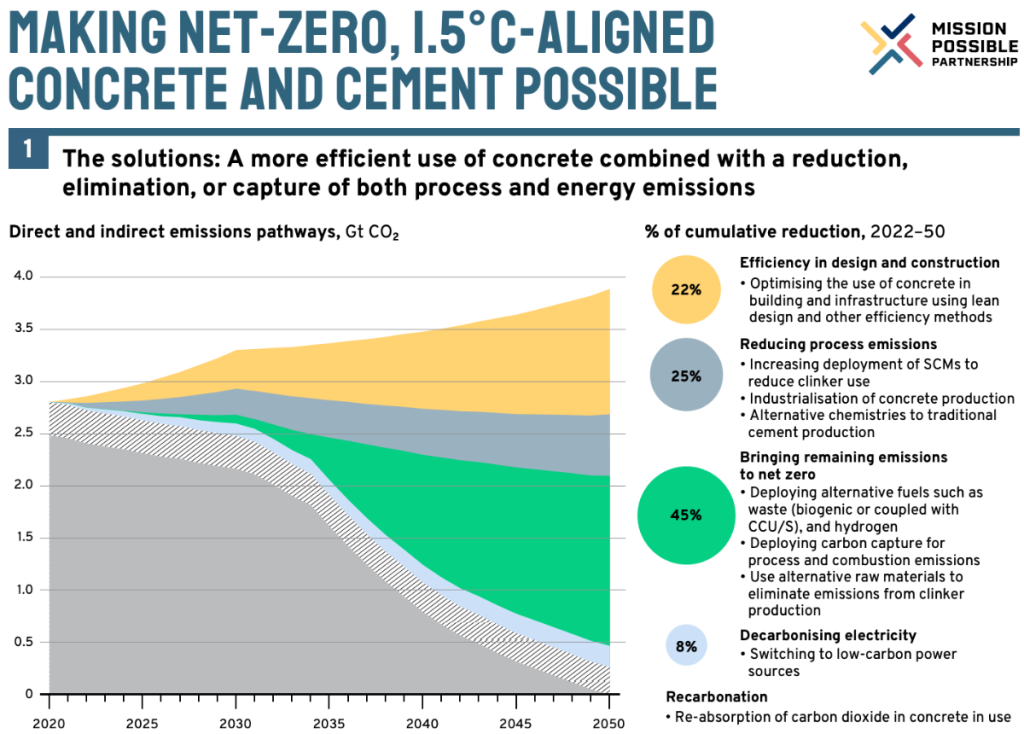

The cement industry has an increasingly clear technological roadmap to decarbonisation through efficiency, alternative fuels and innovative materials underpinned by affordable policy levers.

Cement is primarily made by heating limestone and clay to very high temperatures in a kiln, creating clinker. This is ground with other materials to produce cement powder. Why does it matter? The industry creates about 8% of global CO2 emissions, thanks to the energy-intensive clinker production process and the CO2 released when limestone is converted to clinker.

Today’s cement decarbonisation roadmaps agree on the need for the following four changes:

Massive investment will be needed to transform the cement industry (mainly due to CCUS), and public funding will play an important role in driving the transition. However, many early policy options are available that can help cut emissions with little or no direct financial support.

Impactful policies with limited financial support?

The following three policies all have potential to trigger decarbonised cement production.

Modernising construction codes and standards. Some types of SCMs like limestone filler and blast furnace slag are already common in cement blending to reduce clinker use. However, uptake of blended cements in the construction market has often been impeded by the very slow evolution of building codes and product standards in a conservative industry.

Governments could help by introducing performance-based building codes that allow blended cements in the market when demonstrating certain performance criteria. RMI has recently published a guide with practical recommendations for developing such standards and specifications for concrete.

Untapped waste-to-energy potential. Cement plants can transform industrial and agricultural waste into alternative fuel sources to provide thermal energy for cement manufacturing, with the very high temperatures in this process capable of destroying potentially hazardous residuals.

Although this is already being embraced by many manufacturers, changes in waste regulation can further support the phase-out of fossil fuels by diverting waste streams from simple disposal and recognising it as a viable waste management solution.

For instance, Poland’s cement industry rapidly increased its average thermal substitution rate to 45% in 2011 and above 60% in 2017, due in part to strong enforcement of waste regulations.

Green procurement power. Government purchasing can create market demand for low-carbon construction materials through green public procurement (GPP) policies. With the public sector accounting for 40% to 60% of concrete sales globally, public buyers can impose more stringent sustainability criteria in their projects – and limits on embedded carbon emissions in concrete.

Governments may be well placed to absorb the higher cost, but this can be negligible: A case study published by Ramboll in November 2024 on the construction of a new school building in Zürich, concluded that the inclusion of GPP criteria allowed the reduction of embodied emissions from concrete use by almost 25% for a modest 2% increase in cost.

It’s clear that CCUS remains crucial for the industry’s long-term net-zero ambitions. However, a series of other solutions, including those above, can be deployed more rapidly, provide about 50% of the emissions savings needed, and put the industry on solid footing towards its 2030 target.

This is an abridged version of an article originally written by Elliot Mari of the Industrial Transition Accelerator (ITA) for World Cement.

Sector Transition Strategy: Making Net-Zero, 1.5C-aligned concrete and cement possible, Mission Possible Partnership

Following last month’s focus on Brazilian low-emissions steel as part of the Industrial Transition Accelerator (ITA) Project Support Programme in the country, we’re returning to focus on another sector – Brazil’s chemical industry and particularly, clean ammonia and methanol production.

Brazil’s chemicals sector is the sixth largest globally; however, the country has historically been heavily dependent on imports for ammonia and methanol – commodities that are expected to play a critical role in decarbonising the global chemicals industry. More than 95% of Brazil’s nitrogen fertiliser and 100% of methanol are imported, at an annual cost of around USD 4.8 bn.

At the same time, it is ideally positioned to become a competitive producer and potentially a leading global exporter of low-emission ammonia and methanol by leveraging its significant bioresource base, renewable energy resources, and clean hydrogen potential. Estimates of the current and future levelised cost of green hydrogen (LCOH) around the world have become more conservative in the past 12 months, but nonetheless continue to highlight Brazil as a competitive location, with a projection for the country reaching below US$ 4.5/kg H2 by 2030. Both chemicals have similar options for decarbonised production routes:

The first production route uses renewable electricity and freshwater to produce hydrogen through electrolysis, which is then combined with nitrogen from the atmosphere to produce ammonia or with CO2 to produce methanol. Brazil is particularly well-placed to produce ‘green’ methanol in this way due to its bioresource base and synergies with the existing ethanol industry.

The second route is bio-based, using gasification or reforming of biomass to produce chemical feedstocks, which can leverage Brazil’s degraded land for biomass production and utilise its abundant agricultural residues, particularly from sugarcane. However, this route faces challenges related to the collection of and competition for sustainable biomass as well as competition for land.

The third route involves carbon capture utilisation and storage (CCUS) applied to conventional fossil fuel-based production but is generally not deemed feasible in Brazil in the short term due to high natural gas prices and the large capital investments required for carbon capture, utilisation and storage infrastructure.

Promise and projects

The renewable electricity and bio-based routes are seen as the most promising paths for Brazil to decrease its chemical import dependency and shift towards exporting low-emissions alternatives. In 2022, there were 42 officially registered green ammonia, methanol, hydrogen, and other hydrogen derivatives projects in Brazil. The ITA has selected four of these for further support all of which are targeting FID in the near-term:

ITA has consulted these selected projects in Brazil to identify barriers to FID and potential solutions and is now supporting them in collaboration with existing initiatives and international organisations. This involves mobilising stakeholders to create the necessary conditions for projects to progress towards FID.

Key barriers these projects face include: securing long-term offtake agreements can underpin project financing; navigating an uncertain European export market where the implementation of carbon regulation is gradual and guarantees of scale are hard to come by; managing Brazil’s high cost of capital affecting project economics; and overcoming challenges around infrastructure development, particularly for electricity transmission.

For more on these challenges as well as opportunities to overcome them, you can access the full Brazil Insights Briefing from ITA here, covering five vital industrial sectors. And join us for the final part of this series next month, when we look at Brazil’s SAF and e-SAF potential.

Europe’s healthy project pipeline has the potential to convert into a healthy bottom line

Our Global Project Tracker counts a total of 205 net-zero-aligned industrial projects across Europe. Roughly a quarter have reached final investment decision (FID) or are operational leaving another 158 still in the pipeline, announced but without the finance – representing huge potential waiting to be unlocked. And the current high-fliers of European projects? Over half of Europe’s operational projects are in aviation.

Global Project Tracker, Mission Possible Partnership

Hear more from MPP at events and access tickets on related conferences from our partners.

Thank you for reading, if you enjoyed this newsletter, please share it with your network.

If this edition of Signal was shared with you, you can sign up for our monthly mailings here.

The Mission Possible Partnership Team