November 1st [Washington, DC, London, Geneva, Houston, Los Angeles], the Mission Possible Partnership (MPP) announces the appointment of Faustine Delasalle to the position of Chief Executive Officer (CEO). Effective today, Faustine will lead MPP’s growing portfolio of activities to unlock deep decarbonisation projects in industry, including live programmes in the US and Europe.

The move signals a step-change for the organisation, which was founded in 2019 and recently established as a fully independent not-for-profit entity. With the Board’s backing, Faustine will lead a new strategic phase centered on supporting and unlocking decarbonisation projects across heavy industry and transport sectors, which together account for more than 30% of all global carbon emissions. The goal is to build a critical mass of zero-carbon projects across seven carbon-intensive industries this decade – and get ‘shovels in the ground’ by 2025 for those projects to be up and running by 2030.

MPP milestones for the decarbonisation of these industries – aluminium, concrete, chemicals, steel, aviation, shipping and trucking sectors –, a result of its vision-setting sector transition strategies, reveal the minimum number of projects that must be online in each sector by 2030 to make net zero emissions by 2050 viable. Whilst the pipeline is growing, it is uneven and far short of what is needed, and Final Investment Decisions (FIDs) must be reached on hundreds of projects in the next two-to- three years.

Faustine first conceived that hard-to-abate sectors reaching net zero emissions by 2050 was ‘mission possible’, with colleagues, back in 2018, whilst she was spearheading the growth of the Energy Transitions Commission (ETC). From here, the Mission Possible Partnership was created, with ETC as a founding partner along with RMI, the We Mean Business Coalition, and the World Economic Forum. Faustine has held MPP leadership positions ever since and directly helped to position decarbonisation as a business opportunity with executives and boards of major industrial companies. Today, most big businesses in those sectors have committed to reducing carbon emissions close to zero, with significant cuts already before 2030, and the very first commercial-scale, zero-carbon plants have broken ground.

Jessica Uhl, MPP Co-Chair says, “Faustine continues to be an inspiration with her relentless pursuit of our mission and her ability to experiment to learn new ways to get there. She has such clarity and has already proven that she can deliver impressive breakthroughs in this journey. She is perfectly placed for this new role.”

To unlock green investment in the hard-to-abate sectors, Faustine will now steer MPP in creating a flywheel of collaboration across industry, energy, manufacturing and consumer goods, finance sectors and governments to incubate green value chains and improve the business case of green industry and transport projects. The work will incorporate direct support to flagship projects; orchestrating value chain collaborations – such as the recently announced Transatlantic Clean Hydrogen Trade Coalition, created to enable the first clean hydrogen shipment across the Atlantic by 2026; supporting green industrial hubs in the US and beyond; and building market acceleration platforms to facilitate supply- demand matching at scale for green products. MPP aims to expand its geographical footprint beyond US and Europe.

The clock is ticking to get a major wave of deep decarbonisation projects in heavy industry and transport off the ground. We need to experiment with different approaches to find out how to unlock those investments most effectively. I’m looking forward to leading the organisation in this new phase of action, working closely with our expanding network of partners, including our four founding partners and our strategic partner the Bezos Earth Fund.

Faustine Delasalle, MPP CEO

Together with her team, Faustine is supported by a newly established network of Senior Fellows – comprising recognised leaders from across the corporate landscape, with unique expertise in industries related to the organisation’s work. MPP will also continue to operate as a collaboration platform, partnering up with like-minded organisations across the globe to expand its reach and impact, and facilitate collective learning in the face of the climate emergency. MPP continues to benefit from the support of the Bezos Earth Fund, Breakthrough Energy, and Schmidt Futures.

Dick Benschop, Senior Fellow and MPP Board Member says, “Faustine’s inspirational leadership has already brought incredible progress to the industry. Embracing and embedding collaboration in the decarbonisation space is a true Faustine superpower that has long-benefitted MPP, and we are grateful she will now bring these skills to her role as CEO.”

Prior to joining MPP full-time, Faustine was a Partner at systems-change firm Systemiq and was the Director of the ETC for its first 6 years of operation. She will continue to serve as ETC Vice-Chair. Earlier on, Faustine worked in the public sector, with a career in French politics, incorporating both Parliament and local authorities. She is an alumna of SciencesPo Paris and of the London School of Economics and holds degrees in political sciences and economics.

Geneva, London, Washington DC – The Mission Possible Partnership has announced new leadership appointments effective April 1, as the go-to organisation for decarbonisation of hard-to-abate industry and mobility sectors embarks on a new phase of growth.

Jessica Uhl, previously Vice Chair, will join Chad Holliday as Executive Co-Chair, strengthening MPP’s executive capacity as an independent and trusted adviser to leading corporates, policymakers and other stakeholders. Jessica and Chad will jointly oversee MPP’s pivot from vision-setting to supporting the next wave of deep decarbonisation projects.

Jessica has served as MPP Vice Chair since October 2022. A board director at Goldman Sachs, she serves as strategic advisor to Breakthrough Energy; a member of the executive advisory board of the Columbia Center on Global Energy Policy; and a board member of RMI, one of MPP’s four founding partners. Formerly the chief financial officer of Shell, Jessica has been recognised by Forbes and Fortune as one of the Most Powerful Women in the World.

Chad Holliday said: “On behalf of the board, we’re grateful to Jessica for her commitment and contribution to enhance our organisational capacity and ways of working. We have defined clear, operationally relevant pathways for action in this decade. Jessica and I will work closely to oversee the execution of our industrial decarbonisation programmes at scale, in the US and globally”.

Faustine Delasalle appointed Executive Director of MPP Global

Faustine Delasalle, previously MPP Director of Systems Change and a founding director of the partnership from inception, is appointed Executive Director of MPP Global. She will lead MPP’s efforts to create a supportive market environment for zero-carbon investments and support leading companies in making a first wave of zero-carbon projects reach final investment decisions. She will in particular expand the portfolio of first projects that MPP actively supports beyond the two US hubs where MPP has been operating since 2022.

A seasoned coalition builder and thought leader, Faustine has led distinctive collaborative analysis on the energy transition and has played a central role in the creation of a shared vision for decarbonisation in hard-to-abate sectors across the industry and mobility ecosystem. She was the Director of the Energy Transitions Commission for six years and authored the 2018 ETC report ‘Mission Possible’ which inspired the creation of MPP.

Chad Holliday said: “Leading the development of net zero sector transition strategies endorsed by more than 200 industrial companies, Faustine has been instrumental in positioning MPP as a highly collaborative organisation. On behalf of the MPP Board, I thank Faustine for her rigour and thought leadership in establishing MPP as a trusted, independent partner for industry and policymakers.”

It has been a great privilege to support MPP since its inception, working with industry leaders to define high-ambition, science-based decarbonisation pathways. We are at an exciting juncture, with growing consensus on the way forward and a pipeline of flagship near-zero carbon projects. Our focus now is to see those projects come to fruition in this decisive decade, while expanding the project pipeline at pace.

Faustine Delasalle

Independence and partnership

MPP was incorporated in the United States as an independent, not-for-profit organisation in 2022. The new leadership appointments build on this evolutionary step, marking a new phase in the execution of MPP’s sector strategies to support rapid commercial deployment of First Projects within 1.5 degrees-aligned sectoral carbon budgets.

From April 1, 2023, MPP will become operationally independent of its four founding partners: Energy Transitions Commission, RMI, We Mean Business Coalition and the World Economic Forum. Founding partners will continue to be represented on the MPP Board, and to play an integral role in supporting First Projects as MPP continues to engage a diverse network of stakeholders.

Paul Swinand, previously MPP operations lead, is appointed Treasurer to the MPP Board. Melia Manter, MPP communications manager, is appointed Secretary to the Board. The intention of the Board is to appoint a new CEO before the year-end.

As 2026 gets underway, it is clear this could be a pivotal year, with the building momentum of clean industry shifting from announcements to investment. More projects than ever are in the pipeline and there has been an increase in those hitting final investment decision (FID). The action is diversifying worldwide, opening up opportunities for countries with a smaller existing industrial footprint and prompting discussions among traditional industry leaders.

Included this month:

Mapping the momentum of the growing global clean industry pipeline

Nick Mabey, CEO of E3G, and our CEO, Faustine Delasalle, share why Europe’s industrial future depends on creating lead markets for clean commodities

The ITA continues its country-focused acceleration in India with partnerships to foster green hydrogen and solar scale-up

Clean industry is rising, opportunities for 2026

The global pipeline of clean projects spans 70 countries. Of these, China currently has the single largest share of projects, with more than 200 projects in our Global Project Tracker and 54 projects financed or operating. A rapidly growing renewable power sector and policy frameworks that support clean hydrogen and its derivatives are driving clean commodity production growth across the country.

Outside of China, new opportunities are spreading out; nearly half of investment-ready projects lie in the ‘new industrial sunbelt’, many in emerging economies. This leaves Europe facing a strategic opportunity for renewal. Replacing ageing industrial assets with clean production capacity can revitalise longstanding industrial regions, reinforce energy independence and strengthen industrial competitiveness.

This year is an opportunity for countries worldwide to gain an early mover advantage and turn the wave of 2025’s announcements into solid investments.

Europe’s industrial future depends on creating lead markets for clean commodities

From Faustine Delasalle, CEO, Mission Possible Partnership and Nick Mabey, CEO, E3G

European industry is at a turning point. Fossil-based production has become economically unviable and environmentally unsustainable due to high energy costs, ageing assets and global competition.

High-emission pathways for steel, aluminium and chemicals production in Europe are more expensive than global averages and highly exposed to the price volatility of imported fossil fuels, with European producers steadily losing market share.

Without an urgent shift toward cleaner industrial value chains, Europe risks a slow erosion of its industrial base and with it, the jobs, technologies and strategic influence that underpin its economic strength.

There is room for optimism. The EU boasts one of the world’s most ambitious pipelines of clean industrial projects, but this potential is stalling: of 19 clean industrial plants that secured financing globally last year, only two were in the EU, while China progressed 12.

What’s slowing momentum isn’t technology or capital; it’s the absence of buyers willing to pay a premium for clean materials and chemicals. Without markets for clean commodities, progress in Europe will remain slow at best and, in some cases, is already reversing.

Meeting the competitiveness challenge

While many European companies have announced bold investment plans to decarbonise, Mission Possible Partnership’s Global Project Tracker shows that only a fraction are moving forward. The challenge is clear: unless there is an uptick in demand for clean materials and chemicals, investors will not invest. This is compounded by Europe’s comparatively high energy costs, which further widen the competitiveness gap for clean production.

The European Commission recognised these challenges last year in its Clean Industrial Deal, which put competitiveness and resilience at the centre of Europe’s transition. A few early steps are taking shape – with the proposed extension of the EU Carbon Border Adjustment Mechanism (CBAM) to downstream aluminium and steel intensive products, and new low-carbon steel incentives under the EU tailpipe CO2 regulations for cars.

The next step – the Industrial Accelerator Act, which is due later this month – must now complete this picture by building long-term market certainty that creates a credible business case for low-carbon production.

However, early signals suggest the Act may rely mainly on voluntary labelling and soft incentives. These are welcome, but – like the proposals published in December – are insufficient to create demand at the scale or pace required. And while debates over “Made in Europe” are becoming increasingly contentious, they should not starve the political oxygen for green lead markets. New analysis from the Industrial Transition Accelerator (ITA) and E3G shows what is at stake. Across just four commodities – steel, cement, aluminium and ammonia – Europe already has a pipeline of clean industrial projects worth around €100 billion, but this pipeline is stalled.

Europe’s path to resilience

Investing in these industries is Europe’s path to economic resilience, energy independence and green growth. It is also a cornerstone of Europe’s security strategy: the ability to produce key materials and chemicals domestically strengthens its autonomy in a world where energy and industrial supply chains are increasingly contested. A strong local industrial base also helps ensure a secure domestic defence industry that can scale in times of conflict.

To achieve this, Europe needs a comprehensive lead-markets strategy that mobilises both public and private demand to turn industrial ambition into reality and to maintain the industrial capability to underpin its security. That means deploying a full policy toolkit, tailored to the needs of each sector, from public procurement and contracts for difference to targeted regulation and standards.

Concerns about cost should not hold Europe back. The so-called “green premium” – the extra cost of cleaner materials – has a minimal impact on consumers. For example, switching entirely to clean steel and aluminium would raise the cost of an average car by only 1%. By contrast, dependence on fossil fuels has proven a far greater inflation risk: energy price spikes added roughly six percentage points to EU inflation in 2022 alone.

At the same time, Europe cannot go it alone. Clean energy costs are a critical driver of the competitiveness of clean industry. To make the most of the industrial transition, Europe should tap into the potential of its renewable-rich countries, while building mutually beneficial partnerships with clean energy leaders beyond its borders. Such cooperation can secure affordable clean inputs, strengthen supply chains and expand global green markets, while reinforcing Europe’s diplomatic ties in a world that is increasingly fragmented.

If European leaders want the Clean Industrial Deal to succeed in heralding a new era for European industry, the Industrial Accelerator Act must move beyond good intentions. It should create the strong and predictable lead markets to turn Europe’s clean-industrial ambition into investable demand and secure Europe’s place in the clean economy of the future.

Building connections in India for country-focused acceleration

MPP and the ITA are expanding their networks in India to help bolster the infrastructure essential to accelerating projects to FID. In January, new partnerships were announced with GH2 India to fast-track clean hydrogen and derivative projects to FID and with the International Solar Alliance (ISA).

The GH2 India collaboration is designed to remove practical roadblocks and support India’s emergence as a global leader in clean industrial production. It will focus on stimulating demand, increasing project pipeline visibility, strengthening contracting frameworks and standards to help unlock barriers and push projects towards FID.

“India’s clean industrial transition needs coordinated execution to move projects from intent to investment,” said Nishaanth Balashanmugam, CEO & Director at GH2 India.

The initial priority areas will include:

India–EU collaboration on Renewable Fuels of Non-Biological Origin compliance and certification

Green shipping corridors and offtake dialogues

Expansion of Solar Energy Corporation of India tenders for green fuels

Activating the Clean Industrial Project Tracker to accelerate FID-ready assets

Beyond these, the collaboration will involve stakeholder coordination, technical support on policy, regulation and contracting, as well as fostering public, private corporation, with particular attention on ports and infrastructure.

Scaling solar projects to power clean industry

MPP has joined forces with the International Solar Alliance (ISA), signing a Framework for Action to work with the ITA to help scale and deliver solar projects with a focus on India and Egypt, where there is an abundance of this renewable power source.

The ISA is a global initiative working with 120+ countries to improve energy access and security, advocating the use of solar power as a sustainable transition to a clean energy future.

The partnership will work to speed up solar project deployment through improved coordination and action, drawing on the ISA’s deep expertise and connectivity in energy and infrastructure systems, alongside the ITA’s practical experience of fast-tracking industrial projects.

These Frameworks for Action will strengthen the ITA’s India project support programme to scale clean industrial solutions for the 60+ projects in India’s growing pipeline.

Upcoming events & partnerships

Hear more from Mission Possible Partnership at events and access tickets on related conferences from our partners.

Economist Impact’s 11th annual Sustainability Week, brings together leaders to share case-studies, insights and ideas to drive action on sustainability. With more than 400 speakers, 2,500 in-person attendees, 80 case studies, the event tackles sustainability-related business challenges, finds solutions and gets results.

CATALYZE will assemble the people building the energy and industrial systems of the future. This new flagship summit from ASME and Constructive explores the real-world challenges and opportunities ahead – focusing on action, not just ambition.

Thank you for reading; if you enjoyed this newsletter, please share it with your network. If this edition of Signal was shared with you, you can sign up for our monthly mailings here.

Heavy industry is on the brink of a major transformation. Developing low-emissions products and decarbonizing existing industrial facilities can increase domestic and global economies, protect energy security and resilience, create hundreds of thousands of jobs, and improve the quality of life for people across the planet by reducing pollution and supporting global climate goals.

Enabling the triple bottom line of economy, community, and environment requires a tremendous investment in new projects this decade. Trillions of dollars of capital will be needed in industry and transportation. But financing alone is not enough. Building these projects requires a collaborative ecosystem of project developers, policymakers, community organizations, and financiers to support innovation, sustainability, and economic growth.

Heavy industry and transportation sectors — cement, steel, aluminium, chemical production, aviation, shipping, and trucking — together generate more than 30% of global greenhouse gas (GHG) emissions. Meeting global climate goals will require building more than 700 net-zero industrial projects and deploying 7 million zero-emissions trucks by 2030.1 So far, just 12% of these projects are operational. Most will be in regional industrial hubs, or clusters, where there is a concentration of existing industrial activity and where the physical, social, regulatory, and economic infrastructure is in place to support rapid scale-up. Today, first-of-a-kind (FOAK) and nth-of-a-kind (NOAK) decarbonization projects face tremendous hurdles, but our on-the-ground experience and research show there is a key to unlocking them.

From August 2022 to December 2024, Mission Possible Partnership and RMI, with support from the Bezos Earth Fund, accelerated the development of clean industrial hubs in California and Texas, directly partnering with 18 FOAK clean industrial projects to grow regional economies, strengthen local workforces, and protect energy security while reducing industry’s environmental impacts.

Clean industrial hubs bring together project developers, policymakers, financial institutions, and community-based organizations to advance regional clusters of clean energy and industrial decarbonization projects. These stakeholders work together to benefit the local economy by sharing infrastructure, creating demand for low-emissions fuels and materials, and implementing innovative technology while minimizing environmental impact. Clean industrial hubs help spur economic growth, create employment opportunities, and unlock new technologies.

‘New industrial sunbelt’ countries hold over half of $1.6 trillion global investment pipeline as clean ammonia, critical to food chains, shows signs of being a breakout market

$250 billion of financing already committed to produce clean materials, chemicals and fuels, but a five-fold investment opportunity exists to unlock almost 700 announced projects across the world

Governments in nearly 70 countries can secure early mover advantage by supporting the construction of announced projects through policy measures

China remains the frontrunner in clean industry development, securing a quarter of the $250 billion of investment in clean plants to date, closely followed by the US at 22% and the EU at 14%. But a bloc of emerging markets including India, Egypt and Brazil, part of the ‘new industrial sunbelt’, is quickly catching up to countries with historic industrial bases, according to new data from the Global Project Tracker and accompanying report published today by Mission Possible Partnership (MPP).

The ‘big three’ industrial leaders may soon be overtaken by a host of newly industrialising countries capitalising on favourable conditions for renewable energy production and building momentum in sectors at the forefront of a new clean industrial revolution. This shift points to a potential industrial realignment, as the production of materials, chemicals and fuels moves across geographies and new trade corridors emerge. At the heart of this shift is the industrial sunbelt, a region spanning Africa, Asia and South America where abundant natural resources are being harnessed to provide solar energy and supportive policy environments and cost advantages combine to create ideal conditions for new industrial processes.

Industrial sunbelt countries, such as Indonesia and Morocco, have secured a fifth of investment in clean industrial plants to date. However, a $948 billion investment opportunity exists for their announced projects, particularly as economies dominated by agriculture increasingly see lower-cost clean ammonia for fertiliser as both an economic opportunity and a chance to build increased food security.

The new report, Clean Industry: transformational trends, by MPP and supported by the Industrial Transition Accelerator (ITA) – global alliances focused on advancing clean industry transformation – shows a global $1.6 trillion pipeline of projects announced but not yet financed. Industrial sunbelt countries account for 59% of this investment pipeline, compared to18% for the US, 10% for the EU, and just 6% for China[1]. Projects span key sectors, including aluminium, chemicals, cement, aviation and steel.

In total, a record 826 commercial-scale clean industrial plants across 69 countries are logged in the MPP Global Project Tracker. The growth in this third edition of the Global Project Tracker underscores that companies around the world are continuing to capitalise on clean industrial projects and tap into nascent markets despite ongoing geopolitical and economic uncertainty.

The data shows that of all projects, 69 are operational and 65 have secured financing, with eight reaching final investment decision in the last six months. The remaining 692 projects have been announced but are not yet financed.

Despite increasing competition alongside economic and political headwinds, projects representing $450 billion of investment have been announced in the US and the EU. These countries now face a significant opportunity to enhance investment conditions or risk falling behind. Investment has thrived where projects are supported by stable policies, measures to boost demand, strategic public funding and lower regional capex costs.

The fastest-growing clean industry sectors are green ammonia (28 plants at FID, 344 announced) and sustainable aviation fuels (22 operational plants, seven at FID and 144 announced). Both present a strong business case: with clean ammonia being a drop-in solution for the fertiliser sector – a pre-existing market at scale and sustainable aviation fuels benefit from supported by strong regulatory and policy frameworks as well as a continuing demand for air travel.

CEO of MPP and Executive Director of the ITA, Faustine Delasalle, said: “Just like the industries of yesterday located near the coal mines which powered them, the new generation of energy-intensive industrial plants will go to where they can access abundant, reliable, cheap, clean electricity to produce materials, chemicals and fuels. The industrial heartlands of the past will have to be smart and cooperate if they want to retain their leading positions. MPP’s Global Project Tracker shows a relocation of the industrial base is already underway, with the new industrial sunbelt of the world poised to overtake Western nations in sectors like ammonia, causing major ripples throughout the global economy.”

Christiana Figueres, Co-Founder of Global Optimism, said: “MPPs Global Project Tracker shows that a new Industrial Revolution is on the rise. Perhaps surprisingly, developing economies have an enormous opportunity to leapfrog fossil fuels in heavy industry and transport creating the infrastructure for sustainable economic growth in the 21st century. We now need to unlock the full potential of the clean industrial revolution and exponentially accelerate the existing pipeline.”

The industrial relocation is driven by ammonia, an essential ingredient in fertilisers

Analysis shows the new industrial sunbelt countries host over three quarters of all commercial-scale green ammonia production facilities planned globally (at both FID and announced). As well as its use in fertilisers for agriculture, clean ammonia is used in the manufacturing of explosives and is a clean shipping fuel contender. Decreasing electricity and electrolyser costs[2] in emerging markets within the industrial sunbelt mean several countries are predicted to undercut the cost of fossil-fuel based grey ammonia by 2035. Additionally, green ammonia produced in the sunbelt is expected to cost as little as half the price of that produced in Western Europe or the US, underscoring the importance of access to low-cost renewable energy.

Total pipeline (FID and announced) global green ammonia production capacity from first-mover sunbelt countries could play a significant role in supply chains around the world:

India –8%: enough to fertilise an area almost three quarters of its own landmass

Egypt–7%: enough to fertilise an area twice the size of Egypt

Oman, Mauritania and Chile– 6% each: enough to fertilise a land area equivalent to six Omans

For low- and middle-income economies, the transition represents an opportunity to leapfrog carbon-intensive development, access new export markets and gain a competitive advantage in attracting value-creating industries. The development of domestic clean industrial bases can drive sustainable economic growth, create jobs, strengthen energy and agricultural security, and enable these nations to become significant players in future clean commodity markets.

Dan Ioschpe, COP30 Climate High-Level Champion, said: “As a businessperson I know that the companies around the world who have announced plans for sustainable industrial processes won’t have done so lightly. The Global Project Tracker data shows the scale of corporate ambition and entrepreneurial spirit is high and clearly signals that businesses see this shift to sustainable processes as part of their long-term value creation.

It is also clear that countries in the Global South are going to maximise their generation of renewable competitive energy, which could support the expansion of local value chains and hence, promote their social economic development. We now need to work hard to convert this to action and accelerate solutions on the ground, creating the right conditions for such developments.”

Corporate ambitions outpacing government ambition

The pace of new commercial-scale clean project announcements remains strong, but the report highlights a persistent bottleneck: the conversion from announced projects to final investment decisions is too slow. If the rate of conversion seen in the last six months were to continue, it would take approximately 40 years for all announced projects to begin construction. Unlocking the full pipeline will require a fivefold increase in investment, along with concerted action from governments, financial institutions and corporate buyers.

Governments, in particular, can secure industrial leadership by accelerating project financing through policy measures tailored to their unique resource and economic profile.

Sundus Cordelia Ramli, Chief Commercial Officer, Topsoe, Power-to-X, said: “At Topsoe, we’re supporting the energy transition with our power-to-x solutions. The shift towards cleaner fuel solutions we’re witnessing isn’t incremental – it’s a profound redefinition of energy security, driven by sunlight, wind, and strategic foresight, creating new opportunities for sustainable job creation. Abundant solar and wind resources are reshaping global energy dynamics, turning renewable energy into an advantage for countries around the world. Countries traditionally reliant on energy imports now have unprecedented opportunities for fuel security and even export. Chile’s Atacama Desert, with solar radiation levels about 2.5 times higher than the global average, positions the country as a pivotal green hydrogen hub destined to supply Asia and Europe. Morocco’s ambitious green ammonia projects epitomize this shift, drastically cutting fossil fuel dependence and enhancing geopolitical leverage through renewable energy. India’s ambitious targets, aiming for 500 GW of non-fossil fuel capacity by 2030, underscore its transition from major coal importer to emerging clean energy exporter.”

Additional analysis by MPP and the ITA highlights a range of actions that governments can take, such as fuel standard programmes, carbon pricing and state-backed intermediaries to empower domestic industry to help their countries seize part of this burgeoning economic opportunity. The ITA’s Green Demand Policy Playbook sets out a range of evidence-based policy measures available to governments to spur on further investment in clean industry. Its Green Purchase Toolkit offers support and advice to companies that want to invest in clean industrial products and services.

About Mission Possible Partnership: Mission Possible Partnership (MPP) is an independent non-profit organisation advancing global clean industry transformation. Since 2019, we have been working with some of the most energy-intensive industries – aluminium, cement, chemicals, shipping, aviation and steel – to cut their global GHG emissions. We mobilise business, finance, government and civil society leaders to speed up the shift to clean materials, chemicals and fuels. Having charted sectoral pathways to net-zero, we continue to forge new territory, lifting the barriers to enable a critical mass of clean industrial projects to break ground by 2030. Mission Possible Partnership has people and partners on the ground in North America, Brazil, Europe, the Middle East, North Africa, India and Australia.

About the ITA: The ITA is a global multistakeholder initiative, launched at COP28, to catalyse decarbonisation across heavy-emitting industry and transport sectors, that represent a third of global emissions. With expansive networks across industry, financial institutions, and governments, the ITA brings together global leaders to unlock investment at scale, for the rapid deployment of decarbonisation solutions. Within three years, it aims to significantly grow the pipeline of commercial-scale, clean industrial projects to reduce emissions by 2030 and enable delivery of Paris Agreement-aligned ambition for these sectors. https://ita.missionpossiblepartnership.org/

About the Global Project Tracker: Launching in April 2024, the Global Project Tracker maps this transition against the Sector Transition Strategy-derived near-term milestone of building a critical mass of clean industrial plants. This will drive the production of clean commodities in sufficient volumes to enable their markets to scale while their costs begin to fall. In six-monthly updates, the Tracker geo-plots the pipeline of all known commercial-scale clean industrial plants, marking their deployment across announced, financial investment decision (FID) and in operation statuses.

About the data: with methodology improvements, inclusion of new data sources and capacity-adjusted targets for ‘critical mass’ – direct like-for-like comparisons to previous data is not possible. While every effort has been made to ensure the accuracy and completeness of data related to the Chinese market, it is important to note that certain limitations may exist. The availability and transparency of publicly accessible information in China can vary significantly across sectors. We have taken every practical step to verify and validate the information included in the Global Project Tracker.

Countries where commercial scale clean industrial plants are either operational, financed or announced include:

Algeria Angola Argentina Australia Austria Belgium Bolivia Brazil Bulgaria Canada Chile China Colombia Costa Rica Croatia Denmark Egypt Estonia Europe Finland France Germany Greece

Iceland India Indonesia Ireland Italy Japan Jordan Kazakstan Latvia Lithuania Malaysia Mauritania Mexico Morocco Mozambique Namibia Netherlands New Zealand Norway Oman Pakistan Panama Paraguay

Peru Philippines Poland Portugal Qatar Romania Russia Saudi Arabia Singapore South Africa South Korea Spain Sweden Thailand Trinidad & Tobago Turkey Uganda United Arab Emirates United Kingdom United States Uruguay Uzbekistan Vietnam

Additional quotes:

Nick Studer, CEO of Oliver Wyman, said: “The emergence of the new industrial sunbelt represents a pivotal moment in the global clean industry landscape. Countries like Brazil, UAE, India, and Egypt are not just catching up; they are poised to lead the charge in clean industrial projects, capturing over half of the global investment potential.

This shift not only highlights the resilience and adaptability of emerging markets but also underscores the significant economic opportunities that lie ahead. As these nations step up and announce ambitious projects, they are setting the stage for a more sustainable and competitive future in the global economy.”

CEO of MPP and Executive Director of the ITA, Faustine Delasalle, said: “A clean industrial revolution is already quietly underway on every continent of the world. Progress is being made but we’re experiencing a bottleneck. Projects need a five-fold increase in investment by 2030 to allow the full benefits to flow and unlock a critical mass of clean projects – from steel works, to sustainable aviation fuel plants, to chemical plants for fertilisers and shipping fuels.

“Governments have a key role to play through implementing policy measures that open-up lead markets for clean commodities, derisk investments and stimulate corporate partnerships. This can give countries the competitive edge, access to new markets and strengthen their energy and supply chains.”

[1] It is likely that a significant number of planned Chinese projects have not been publicly announced. [2] Mission Possible Partnership, June 2025, Clean Industry: Transformational Trends.

Electrolytic or “green” hydrogen has garnered significant interest for its potential to reduce emissions across industrial sectors such as steelmaking and fertiliser manufacturing. As the interest in green hydrogen grows, so does the need for robust renewable energy accounting methods to ensure it is produced responsibly.

RMI has emphasised the need for the Inflation Reduction Act’s hydrogen production 45V tax credit to maintain hourly matching over an annual matching to ensure climate-aligned emission profiles. Hourly matching requires hydrogen production to align its electricity consumption with clean electricity generation on a real-time, hourly basis. Annual matching instead aggregates the total electricity consumption on an annual basis, allowing consumers to claim “clean energy” for hours where there is limited clean generation on the grid. Designing projects that are economically viable while achieving consistent clean power is one of the foremost challenges of the energy transition. If hydrogen developers can find a pathway to competitive business models for hourly matched electrolytic hydrogen, they will establish themselves as an example for industrial decarbonisation efforts more broadly.

So far, much of the discourse on this topic has focused on whether the hourly matching requirement in the 45V tax credit guidance should be upheld. The 2024 presidential election increased tax credit uncertainty, but there are still important reasons for developers to pursue hourly matched power procurement. Accessing international markets is still critical to sustaining green hydrogen business models at scale, for example, and even in domestic markets, relaxing emissions standards makes it harder for offtakers to verify the climate attributes of the product. As such, attention should be given to the inherent costs and risks of power procurement and how the market could transform to address them.

The chart below shows the impact on the price of various project configurations adjusted up or down by 30 percent. Many factors have an impact on the price of hydrogen, but the cost of power remains the single largest driver of hydrogen production economics. Additionally, the amount of power procurement needed remains a substantial bankability risk for many projects. Contracting large volumes of power to ensure high quality climate attributes not only exposes projects to power market risk, but also creates a dependency on regulations that could change in the future. Some configurations may be more insulated from these risks than others.

Even well-informed third parties often struggle to challenge claims about the sustainability of these projects and verify the environmental attributes embedded in the final product. The complexity of hydrogen production, project development uncertainties, and the nascency of the industry make it difficult for policymakers and other stakeholders to understand what asset-level configurations are truly feasible within the proposed policy environment.

As part of an effort to better understand barriers to final investment decision (FID) in Gulf Coast Industrial Hubs, RMI, as part of its work with Mission Possible Partnership (MPP), evaluated power procurement risks and challenges for a hypothetical green hydrogen project in Texas and proposed policy and market-based paths forward for green hydrogen. This work is part of RMI and MPP’s U.S. Hubs program, in partnership with the Bezos Earth Fund.

Power configurations and associated risks

Four different archetypes for procuring clean power were examined for the purposes of green hydrogen developments. These are not the only options to configure power for hydrogen projects, but are representative of common selections:

Behind-the-Meter (BTM): Hydrogen producer has on-site renewables to provide both Energy Attribute Credits (EACs) and direct transmission of power. The renewable and hydrogen production project can be financed together, or ring fenced through an onsite PPA.

Offsite Physical Power Purchase Agreements (PPAs): The hydrogen producer receives all electricity from offsite renewables. The renewables developer “passes” renewable electricity (and associated EACs) to the hydrogen project through the utility for a fee paid by the hydrogen project.

Hybrid: Projects combine multiple power procurement strategies. For example, a project could opt for a hybrid system with on-site anchor renewables plus a supplemental vPPA to increase resource diversity.

Unbundled EAC purchases, decoupled from physical power transactions may be possible for hybrid systems over time, either traded in a market or secured via longer-term contracts.

Risks associated with power procurement

When contracting renewable energy, hydrogen producers must balance the risk of excess production against maintaining supply certainty. Power configurations carry different exposures to the risks and opportunities. For example, behind the meter offers certainty in electricity costs and simplified operations but faces greater weather variability and project dependence. Virtual and physical PPAs can be subject to curtailment and mismatches in hourly production but have the potential for greater resource diversity with hydrogen production and renewables in different locations. Finally, a hybrid configuration can balance the risks but requires more complex alignment between parties. Key risks for each configuration are summarised in the following table and discussed in further detail the subsequent section.

To ensure tax credit compliance, hydrogen developers will need to work with offtakers, regulators, and financial institutions to propose creative solutions through novel contract provisions, project configurations, or additional support to mitigate risks and guarantee high-quality climate attributes. Given the importance of power for electrolytic hydrogen, the following sections will describe some of the risks associated with power procurement and potential solutions.

Risk 1: Weather variability

The challenge

Renewable electricity markets are subject to considerable supply volatility, driven by the variable availability of solar and wind resources. This variability creates a challenge for hydrogen producers aiming to transform renewable resources into stable tax credit revenue for investors and predictable production volumes for offtakers with strict operating constraints.

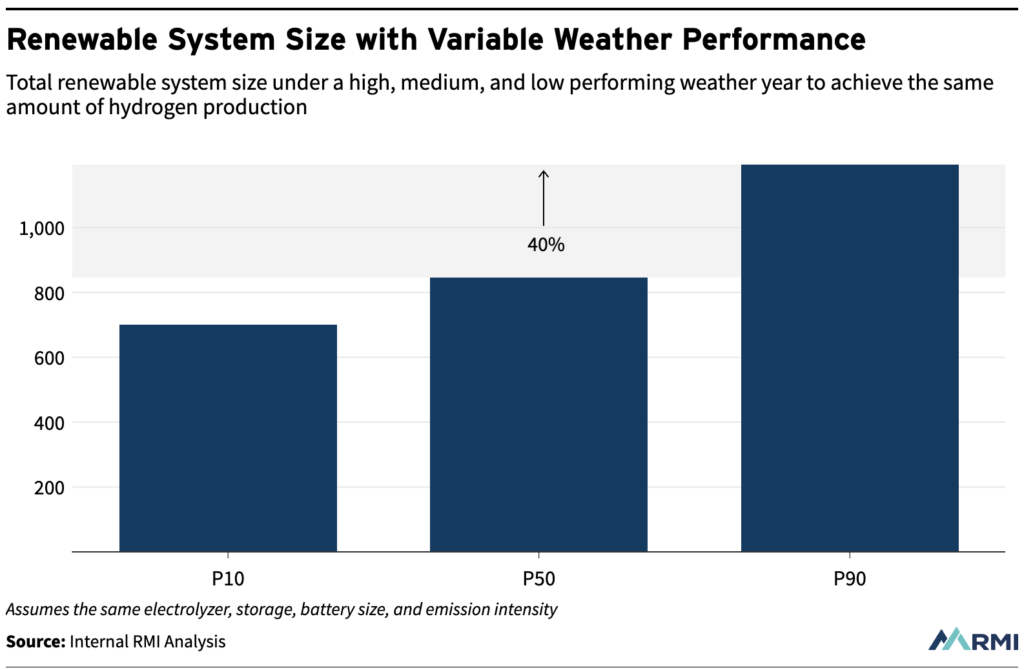

Until other cost reductions and efficiency improvements are achieved, US-based green hydrogen projects will heavily rely on the $3/kg tax credit to maintain economic viability. At the same time, investors require developers to secure upfront offtake contracts to receive financing, and many offtakers require fixed volume delivery due to their own operational limitations. Hydrogen producers must balance fulfilling their fixed offtake obligations with ensuring that every hour of hydrogen production is matched with an hour of clean power consumption to receive the tax credit and guarantee high-quality climate attributes. Producers may choose to structure contracts such that enough power is procured to meet production requirements in the worst weather conditions they may face over the life of the project. As a result, developers may ultimately contract 40 percent more power than they would secure if they planned projects for average weather conditions.

If the system is not sized correctly for poorer weather performance years, reduced renewable capacity factors will force producers to choose between reducing tax credit revenue by using higher carbon intensity grid power, and creating production shortfalls by ramping down their electrolysers, which could violate their contractual obligations. Figure above demonstrates this trade-off. RMI has advocated for the inclusion of an hour-by-hour calculation exception that would reduce the consequences of using grid power to ensure delivery of contracted volumes. The hour-by-hour calculation could preserve the environmental attributes and global competitiveness of the product more effectively than an annual matching approach, while also mitigating the worst consequences of hourly matching. Although conservative renewables contracting could lead to excess production that could be turned into surplus revenue, developers may struggle to monetise the extra volumes in the absence of a liquid market, potentially impacting the bankability of the overall project configuration.

Potential solutions

The challenge of renewable energy variability is not unique to hydrogen. Many other sectors, from data centres to electric utilities themselves, are searching for ways to ensure consistent, reliable power from zero-carbon sources. Some solutions to this challenge may be structural, like pairing oversized hydrogen production systems with electricity or hydrogen storage to store excess power or hydrogen during high-output periods and provide backup during low-output times. However, this kind of solution can be costly and may not lead to a competitive product. First-of-a-kind business model solutions, such as those highlighted below, may be better suited to address this challenge.

Insurance products can provide coverage for losses associated with production shortfalls, performance penalties, or tax credit revenue loss for operational or environmental liabilities. The market for hydrogen-specific insurance is underdeveloped with a potential for high premiums that negatively impact the economics of the solution, but government or concessionary capital support for subsidised premiums, first loss capital for insurance pools, or tax incentives for insurers could catalyse the development of the insurance industry.

Flexible hydrogen contracts with variable offtake agreements can a) empower electrolyser operators to pursue dynamic business models that optimise hydrogen and renewable power sales or b) monetise excess production. Many hydrogen offtakers currently lack the operational flexibility to ramp production but advancements in hydrogen storage or technologies in key offtake sectors could address this gap.

Power guarantees from the renewable developer to provide a minimum quantity of hourly EACs could provide more predictability. However, guarantees may be challenging to negotiate and could increase supply contract costs. The development of secondary power or EAC markets could help optimise the distribution of risk.

Risk 2: Logistic complexity

The challenge

Green hydrogen developers face significant project design and execution complexities, as they navigate construction and operation of renewable power and electrolysis assets. The current 36-months vintage component requires near simultaneous construction of assets, while the hourly matching requirement necessitates closely coordinated operation. This means that both the renewables project and the hydrogen project are dependent on the success of another project that is itself uncertain.

Developers who opt to build behind-the-meter renewables to meet this requirement face a double-sided challenge often referred to as “project on project risk.” In this archetype, hydrogen production is contingent upon the timely completion and operation of the associated renewable project. Likewise, the renewables project is dependent on the timely completion of the hydrogen project for revenue. If either project experiences delays, the profitability of the other will be at risk. The nascency of the industry creates a high risk that hydrogen projects will not be built on time or will be smaller than originally planned.

Developers who opt for vPPAs or PPAs face a similar challenge, though the risk is spread between the hydrogen and renewables developers. The renewable energy supplier’s financing could face hurdles if the hydrogen project is the sole offtaker. In regions with high-performing renewables, there will also likely be intense competition for resources from other high willingness-to-pay industries. Renewables developers may favour these alternative buyers because hydrogen projects are seen as a risky source of revenue.

In addition to the challenge of simultaneous asset construction, vPPA and PPA configurations must also coordinate simultaneously with the asset operations of the power producer and the offtaker. Electrolyser operators need to juggle multiple data feeds, integrating fluctuating real-time price reports, weather conditions forecasts, and real-time operations data from their renewable energy assets so they can quickly ramp production down if renewables stop producing. Errors in this data could lead to a substantial tax credit loss if renewables stop producing due to forecasting errors or technical malfunctions but the electrolyser continues to consume electricity.

Potential solutions

To mitigate project on project risk:

BTM developers could adopt a phased approach, first constructing renewables and integrating hydrogen production integrated later. This would likely require the developer to find another offtaker for their renewable power to provide revenue before the hydrogen project comes online.

PPA and vPPA developers can explore novel power contracting approaches, such as partnering with existing large buyers, like technology companies, as a paired offtaker. This approach can help mitigate risk for renewable developers by avoiding the uncertainties associated with aligning their projects with an emerging industry like hydrogen.

Cross-collateralisation of a portfolio of smaller first-mover projects could reduce the likelihood that isolated errors in any single project will substantially disrupt cashflows to project owners.

Emerging data management solutions to streamline simultaneous operation risk are already being explored by power market service providers.

Risk 3: Grid volatility & uncertainty

The challenge

Hydrogen project developers with grid-connected projects (vPPA, PPA, or hybrid) can face uncertainty from the short-term, minute-to-minute, hour-to-hour, and month-to-month volatility of the electricity market as well as from the rapidly evolving long-term, year-over-year electricity price environment. To protect against the different temporal dimensions of market volatility, developers can secure physical PPAs or vPPAs, (or opt for behind-the-meter systems, which are largely insulated from all the risks described in this section), but there are trade-offs for either option.

Physical PPAs limit the risk of short-term volatility by delivering power at a pre-determined cost with exposure to wholesale price uncertainty only in the sale of excess contracted power back to the grid. However, in the long term, developers risk their projects becoming uncompetitive if PPA prices significantly decline over time.

vPPA configurations experience greater risk from short-term varying power costs because they are exposed to the wholesale market via the contract for differences settlement (CfD) and to the commercial rates via their physical power purchases from the utility. The CfD settlement, which will provide additional revenue to the hydrogen project when prices are high, creates a hedge against long-term increases in the commercial market price, as long as the wholesale price is driven up by the same factors. However, changes in the grid’s energy sources over time can weaken the correlation between the CfD and the commercial prices creating the potential for hedging strategy failures. The first figure above demonstrates the uncertainty in future price evolution reported by ERCOT itself. The second figure above shows the potential consequences of failing to manage wholesale price volatility. A single month in which the average cost of power is more than $160/MWh, as shown in August of 2023, could do irreparable damage to project economics.

Additionally, grid-connected projects may face significant delays due to interconnection queues, as they depend on timely grid access to start production with EACs. Curtailment risks can further complicate hydrogen production, as solar or wind farms can be forced to scale back operations when grid capacity is exceeded, leaving excess energy unused and potentially missing hours of matching EAC.

Potential solutions

To mitigate grid-related risks, the following market and policy solutions exist:

Build onsite renewable or contract with projects physically close to reduce grid exposure and the risks of curtailment at different nodes within the grid. This can be for part or all the electrolyser capacity but may increase weather variability risk.

Enter contracts with retail energy providers to fix electricity consumption costs. These are likely only widely available in deregulated markets and are subject to term negotiation. They could reduce costs vs traditional retail rates if the developer is able secure value for being a flexible load.

Collaborate with Regional Transmission Organisations and federal or state policymakers to streamline grid interconnection processes and identify areas in the system that would benefit from both additional capacity and a large flexible load like a hydrogen plant.

Support development of spot hourly EACs to provide an additional, more liquid source of hourly EACs to enable production during times of supply-driven curtailment.

Next steps

As tax credit uncertainty increases, developers and offtakers alike must proactively address the risks that will persist regardless of regulatory outcomes. Challenges such as weather variability, logistics complexity, and the future of the grid will endure even after final rules are in place. Many market-driven solutions exist, but these investments are costly, high risk, and have long lead times that may necessitate additional government support. Stakeholders can begin collaborating to identify and mitigate these risks, accelerating project deployment once the guidance is released.

Ocean ports around the world represent major sources of coastal air pollution, with fossil fuel-powered ships, trucks, and heavy equipment in use at port terminals.

In Southern California, home to two of the busiest container ports in the county, that pollution is a particularly acute challenge given the proximities to large metropolitan populations. In fact, the Ports of Los Angeles and Long Beach moved more than 16 million TEUs, or nearly 40 percent of imported containers, in the United States in 2023. Those containers include everything from clothes to lifesaving medical equipment. When containers arrive on US shores, they rely on a network of heavy-duty infrastructure known collectively as cargo handling equipment to get them off boats and ultimately into consumer hands.

Cargo handling equipment, also known as container handling equipment, refers to the cranes, top handlers, forklifts, and tractors that load and unload shipping containers on and off boats. Today, most cargo handling equipment runs on diesel. Replacing diesel cargo handling equipment with zero emissions alternatives will improve local air quality and health in neighbouring communities and reduce climate impacts.

RMI and the Mission Possible Partnership analysed the total cost of ownership for four types of cargo handling equipment

But roadblocks remain, including a lack of data to support terminal operators, ports, labor unions, and other key stakeholders in making decisions about technology pathways and plans for needed charging and hydrogen refueling infrastructure.

That’s why RMI and the Mission Possible Partnership analysed the total cost of ownership for four types of cargo handling equipment: to provide stakeholders with an understanding of the zero-emissions technologies available today, how the total cost of battery electric and hydrogen-powered equipment compare with diesel powertrains, and the green electricity and hydrogen needed at the port to power net-zero equipment.

Addressing cargo handling equipment is essential for decarbonising POLA and POLB

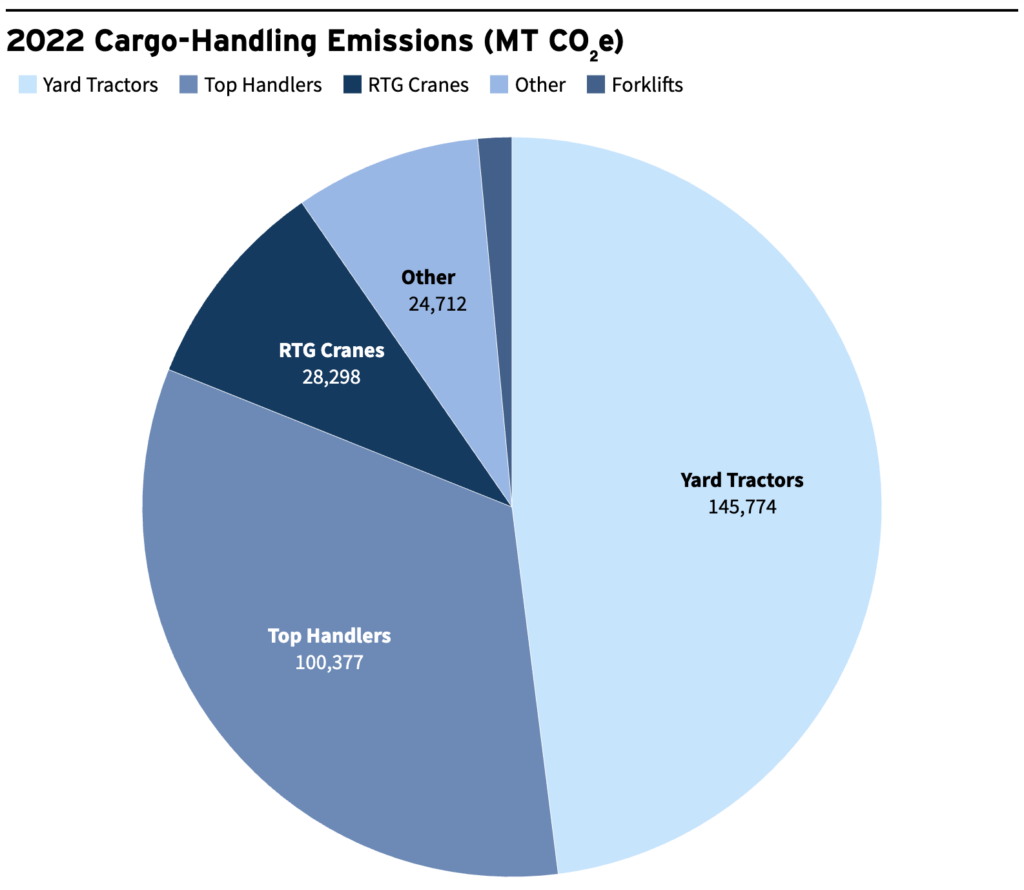

It’s impossible to decarbonise ports without a focus on cargo handling equipment. While most port emissions come from heavy-duty vehicles and ocean-going vessels, cargo handling equipment still accounts for more than 15 percent of port emissions at POLA and POLB. The majority of cargo handling equipment emissions come from two tools: top handlers and yard tractors. Of the more than 3,000 pieces of cargo handling equipment in operation at the ports, yard tractors (48 percent), forklifts (17 percent), top handlers (12 percent), and rubber-tired gantry (RTG) cranes (5 percent) continue to use primarily diesel internal combustion engine technology.

Exhibit 1. Ports of Los Angeles and Long Beach Combined Emissions Profile

The good news is technology readiness levels (TRLs) are improving for zero-emissions cargo handling equipment. Across all cargo handling equipment types, battery electric powertrains have the highest TRL when considering battery electric and hydrogen fuel cell solutions across four types of cargo handling equipment. However, it’s important to note that other factors including space constraints, operational profiles, electricity and hydrogen distribution infrastructure availability, and labour/end-user preferences all influence operator technology choice.

Exhibit 2. Technology readiness levels for battery electric and hydrogen fuel cell cargo handling equipment by type

Zero-emissions yard tractors and RTG cranes are cost-competitive with diesel today

As technologies improve, zero-emissions cargo handling equipment is becoming cost-competitive with its diesel-powered counterparts.

RMI and MPP calculated the 12-year total cost of ownership (TCO) of the four equipment types, considering diesel, electric, and hydrogen powertrains for each. The TCO considers upfront vehicle purchase price and infrastructure costs as well as long-term factors such as maintenance and fuel. California state incentives offered through the Low Carbon Fuel Standard (LCFS) program and Clean Off-Road Equipment (CORE) Voucher Incentive Project are also included.

Exhibit 3. 12-year total cost of ownership (TCO) of four cargo handling equipment types, considering diesel, electric, and hydrogen powertrains – Click to view the table full size

We find that zero-emissions yard tractors and RTG cranes are cost-competitive with diesel today (Exhibit 3).

Overall, hydrogen powertrains appear economically competitive with battery-electric models for yard tractors and high-capacity forklifts, with hydrogen top handlers being significantly more expensive than their electric counterparts. The TCO of hydrogen RTG cranes was not evaluated due to that market segment already being captured by electric models.

Hydrogen yard tractors require more fuel expenditure than electric models, but this cost can be offset because hydrogen units benefit from lower upfront purchase prices after incentives are applied, making both powertrains competitive with diesel. Electric and hydrogen top handlers are both more expensive than diesel due to their large upfront pricing not being sufficiently mitigated by purchase incentives. Hydrogen forklifts are competitive with electric due to reduced infrastructure costs, but both alternative fuel vehicles are much more expensive than diesel, largely due to high upfront purchase prices. Electric RTG cranes are competitive with diesel due to the technology’s maturity and the support of purchase incentives.

However, these findings need to be verified with additional study. Publicly available data on model pricing and maintenance costs are sparse, with hydrogen fuel prices and infrastructure costs also largely uncertain.

Public and private finance can come together to enable turnover of cargo handling equipment

Across the fleet of cargo handling equipment at the San Pedro Bay Ports, RMI analysis shows replacement or conversion of remaining CHE to zero-emissions will cost more than $2.5 billion depending on the split between hydrogen and electric equipment. Results from the same analysis of total costs across POLA and POLB under a mixed scenario — comprising both hydrogen and electric powertrain replacements for existing equipment — would require more than $1 billion to replace 1,500 yard tractors and more than $900 million to replace 400 top-handlers. By comparison, of POLA’s $2.6 billion annual budget, only $15 million is allocated toward zero-emissions port electrification.

Terminal operators and other developers can leverage incentives and research tools like the RMI DIRT tool to identify appropriate cost-saving measures to reduce costs on the path to net zero. Federal tax incentives for the purchase of qualifying new equipment can reduce the per-unit capital expenditure by up to $40,000 even before factoring in upstream production and manufacturing tax credits from the Inflation Reduction Act. California has additional incentives that can reduce the purchase price of new cargo handling equipment by 30 to 55 percent, depending on the vehicle and powertrain.

Additionally, many terminals at US ports are owned by financial institutions or beneficial cargo owners (BCO) who can leverage private capital for the transition. For example, financial institution owners of port terminals could leverage collateralised loans or OEM-backed financing for equipment purchases across multiple facilities to reduce procurement costs. Additionally, common facility ownership at ports presents an opportunity to jointly procure equipment, creating economies of scale.

Systems planning for green electricity and hydrogen must start now to meet the ports’ 2030 goal

Replacing existing diesel cargo handling equipment with net-zero alternatives will require significant volumes of green electricity and/or green hydrogen to be delivered to ports.

Upgrades will be necessary for electrical grid infrastructure serving the ports to accommodate the increased load from recharging hundreds of pieces of equipment, like the upgrades Southern California Edison are already planning for a new transmission-level substation and other grid enhancements to serve an expected increase in demand at POLB. Infrastructure for hydrogen delivery and refuelling will also be necessary to ensure cost-effective delivery of zero-emissions fuel.

Terminal operators may also face site constraints in addition to limited electric capacity. Electric refuelling infrastructure often requires more space than diesel pumps because one electric charger supports fewer vehicles than a diesel pump. These chargers can also present a spike in site-wide power usage, and the lead time for getting the power capacity upgrades at a site to support charger installation can be significant. Similarly, building hydrogen refuelling infrastructure and securing low-cost hydrogen will require coordination across terminal operators and other buyers of hydrogen for trucking and shipping.

Conclusion: Decarbonising goods movement in the United States and beyond

Converting to zero-emissions cargo handling equipment is just one piece of decarbonising ports and goods movement. Actors across the value chain — beneficial cargo owners, terminal operators, ports, OEMs, utilities, and energy suppliers — all have a role to play in ensuring a rapid and cost-effective transition. Further, environmental justice groups are advocating for a transition away from diesel, while labour groups are working to ensure the transition does not displace union jobs. Cargo owners are increasingly interested in choosing carriers with more sustainable operations, creating pressure for fleets to decarbonise.

Maritime trade will continue to be an essential part of our modern way of life, but we can diminish its climate impact. Reducing port emissions in the United States and globally is essential to meeting climate goals, decarbonising goods movement, and reducing harmful pollution in neighbouring communities.

About Clean Industrial Hubs

The insights discussed above come from Mission Possible Partnership and RMI’s Clean Industrial Hub in Los Angeles, California, which accelerates industrial and heavy transportation decarbonisation in the region. Clean industrial hubs bring together policymakers, financial institutions, project developers, and community-based organisations to enable ground-breaking decarbonisation projects in the hardest-to-abate sectors. In Los Angeles, MPP and RMI’s analyses, convenings, and tools support stakeholders working to advance zero-emissions trucking, low-carbon cement plants, sustainable aviation fuel, and decarbonised ports by increasing the size, scale, and speed of critical climate investments that benefit the environment, the economy, and communities. This work is done in partnership with the Bezos Earth Fund.

Our on the ground experience supporting project developers in California and Texas has led us to uncover five critical insights on how to unlock investment in green industrial projects globally:

Technology An economically viable path to decarbonisation is in sight in some sectors.

Demand Projects which rely on mandates progress faster due to an even playing field and longer-term demand certainty.

Infrastructure Achieving decarbonisation goals for industry will require a rapid buildout of industrial assets and infrastructure.

Communities Community engagement is critical to project success and innovative tools can elevate engagement.

Finance Financiers must explore more innovative deal structuring to efficiently share risks in complex projects.

We are on the cusp of a clean industrial revolution. The world is transforming how it produces the materials, chemicals and fuels we all rely on.

Clean industry is coming. Those who act now can capture a trillion-dollar opportunity – building stronger economies, more resilient supply chains, creating new jobs, securing greater energy and food security, and leading the industries of the future.

We are on the cusp of a clean industrial revolution. The world is transforming how it produces the materials, chemicals and fuels we all rely on.

Clean industry is coming. Those who act now can capture a trillion-dollar opportunity – building stronger economies, more resilient supply chains, creating new jobs, securing greater energy and food security, and leading the industries of the future.