Introduction

Electrolytic or “green” hydrogen has garnered significant interest for its potential to reduce emissions across industrial sectors such as steelmaking and fertiliser manufacturing. As the interest in green hydrogen grows, so does the need for robust renewable energy accounting methods to ensure it is produced responsibly.

RMI has emphasised the need for the Inflation Reduction Act’s hydrogen production 45V tax credit to maintain hourly matching over an annual matching to ensure climate-aligned emission profiles. Hourly matching requires hydrogen production to align its electricity consumption with clean electricity generation on a real-time, hourly basis. Annual matching instead aggregates the total electricity consumption on an annual basis, allowing consumers to claim “clean energy” for hours where there is limited clean generation on the grid. Designing projects that are economically viable while achieving consistent clean power is one of the foremost challenges of the energy transition. If hydrogen developers can find a pathway to competitive business models for hourly matched electrolytic hydrogen, they will establish themselves as an example for industrial decarbonisation efforts more broadly.

So far, much of the discourse on this topic has focused on whether the hourly matching requirement in the 45V tax credit guidance should be upheld. The 2024 presidential election increased tax credit uncertainty, but there are still important reasons for developers to pursue hourly matched power procurement. Accessing international markets is still critical to sustaining green hydrogen business models at scale, for example, and even in domestic markets, relaxing emissions standards makes it harder for offtakers to verify the climate attributes of the product. As such, attention should be given to the inherent costs and risks of power procurement and how the market could transform to address them.

The chart below shows the impact on the price of various project configurations adjusted up or down by 30 percent. Many factors have an impact on the price of hydrogen, but the cost of power remains the single largest driver of hydrogen production economics. Additionally, the amount of power procurement needed remains a substantial bankability risk for many projects. Contracting large volumes of power to ensure high quality climate attributes not only exposes projects to power market risk, but also creates a dependency on regulations that could change in the future. Some configurations may be more insulated from these risks than others.

Even well-informed third parties often struggle to challenge claims about the sustainability of these projects and verify the environmental attributes embedded in the final product. The complexity of hydrogen production, project development uncertainties, and the nascency of the industry make it difficult for policymakers and other stakeholders to understand what asset-level configurations are truly feasible within the proposed policy environment.

As part of an effort to better understand barriers to final investment decision (FID) in Gulf Coast Industrial Hubs, RMI, as part of its work with Mission Possible Partnership (MPP), evaluated power procurement risks and challenges for a hypothetical green hydrogen project in Texas and proposed policy and market-based paths forward for green hydrogen. This work is part of RMI and MPP’s U.S. Hubs program, in partnership with the Bezos Earth Fund.

Power configurations and associated risks

Four different archetypes for procuring clean power were examined for the purposes of green hydrogen developments. These are not the only options to configure power for hydrogen projects, but are representative of common selections:

- Behind-the-Meter (BTM): Hydrogen producer has on-site renewables to provide both Energy Attribute Credits (EACs) and direct transmission of power. The renewable and hydrogen production project can be financed together, or ring fenced through an onsite PPA.

- Virtual Power Purchase Agreements (vPPAs): The hydrogen producer contracts a vPPA with a renewables developer to receive EACs and a contract for differences (CFD) settlement, or the financial settlement between the market price and the agreed strike price. The hydrogen producer receives all electricity from the grid through a separate contract with the local utility.

- Offsite Physical Power Purchase Agreements (PPAs): The hydrogen producer receives all electricity from offsite renewables. The renewables developer “passes” renewable electricity (and associated EACs) to the hydrogen project through the utility for a fee paid by the hydrogen project.

- Hybrid: Projects combine multiple power procurement strategies. For example, a project could opt for a hybrid system with on-site anchor renewables plus a supplemental vPPA to increase resource diversity.

- Unbundled EAC purchases, decoupled from physical power transactions may be possible for hybrid systems over time, either traded in a market or secured via longer-term contracts.

Risks associated with power procurement

When contracting renewable energy, hydrogen producers must balance the risk of excess production against maintaining supply certainty. Power configurations carry different exposures to the risks and opportunities. For example, behind the meter offers certainty in electricity costs and simplified operations but faces greater weather variability and project dependence. Virtual and physical PPAs can be subject to curtailment and mismatches in hourly production but have the potential for greater resource diversity with hydrogen production and renewables in different locations. Finally, a hybrid configuration can balance the risks but requires more complex alignment between parties. Key risks for each configuration are summarised in the following table and discussed in further detail the subsequent section.

To ensure tax credit compliance, hydrogen developers will need to work with offtakers, regulators, and financial institutions to propose creative solutions through novel contract provisions, project configurations, or additional support to mitigate risks and guarantee high-quality climate attributes. Given the importance of power for electrolytic hydrogen, the following sections will describe some of the risks associated with power procurement and potential solutions.

Risk 1: Weather variability

The challenge

Renewable electricity markets are subject to considerable supply volatility, driven by the variable availability of solar and wind resources. This variability creates a challenge for hydrogen producers aiming to transform renewable resources into stable tax credit revenue for investors and predictable production volumes for offtakers with strict operating constraints.

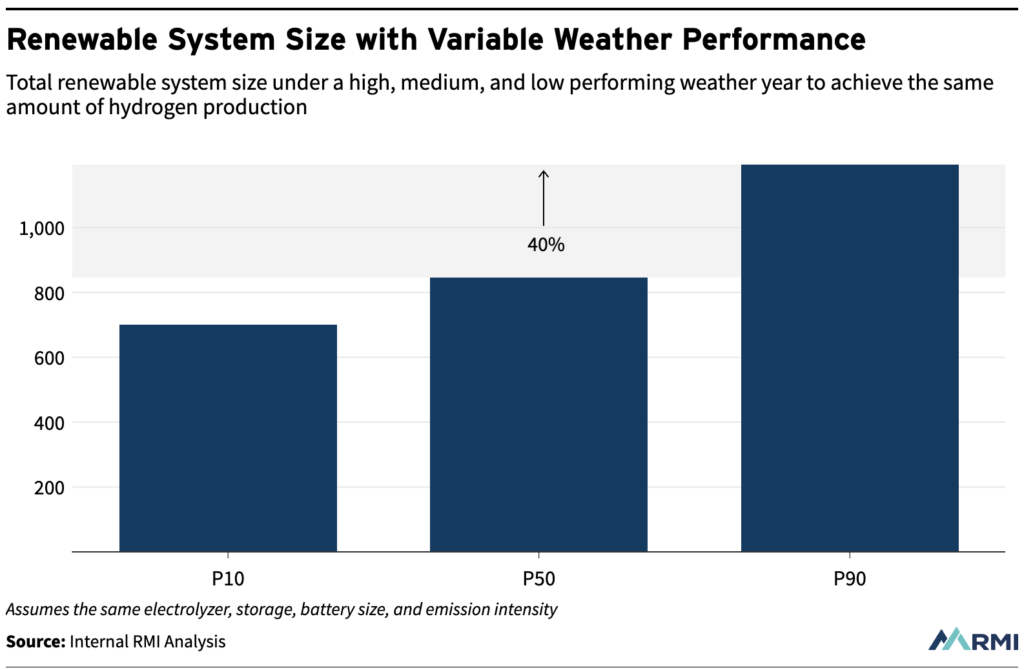

Until other cost reductions and efficiency improvements are achieved, US-based green hydrogen projects will heavily rely on the $3/kg tax credit to maintain economic viability. At the same time, investors require developers to secure upfront offtake contracts to receive financing, and many offtakers require fixed volume delivery due to their own operational limitations. Hydrogen producers must balance fulfilling their fixed offtake obligations with ensuring that every hour of hydrogen production is matched with an hour of clean power consumption to receive the tax credit and guarantee high-quality climate attributes. Producers may choose to structure contracts such that enough power is procured to meet production requirements in the worst weather conditions they may face over the life of the project. As a result, developers may ultimately contract 40 percent more power than they would secure if they planned projects for average weather conditions.

If the system is not sized correctly for poorer weather performance years, reduced renewable capacity factors will force producers to choose between reducing tax credit revenue by using higher carbon intensity grid power, and creating production shortfalls by ramping down their electrolysers, which could violate their contractual obligations. Figure above demonstrates this trade-off. RMI has advocated for the inclusion of an hour-by-hour calculation exception that would reduce the consequences of using grid power to ensure delivery of contracted volumes. The hour-by-hour calculation could preserve the environmental attributes and global competitiveness of the product more effectively than an annual matching approach, while also mitigating the worst consequences of hourly matching. Although conservative renewables contracting could lead to excess production that could be turned into surplus revenue, developers may struggle to monetise the extra volumes in the absence of a liquid market, potentially impacting the bankability of the overall project configuration.

Potential solutions

The challenge of renewable energy variability is not unique to hydrogen. Many other sectors, from data centres to electric utilities themselves, are searching for ways to ensure consistent, reliable power from zero-carbon sources. Some solutions to this challenge may be structural, like pairing oversized hydrogen production systems with electricity or hydrogen storage to store excess power or hydrogen during high-output periods and provide backup during low-output times. However, this kind of solution can be costly and may not lead to a competitive product. First-of-a-kind business model solutions, such as those highlighted below, may be better suited to address this challenge.

- Insurance products can provide coverage for losses associated with production shortfalls, performance penalties, or tax credit revenue loss for operational or environmental liabilities. The market for hydrogen-specific insurance is underdeveloped with a potential for high premiums that negatively impact the economics of the solution, but government or concessionary capital support for subsidised premiums, first loss capital for insurance pools, or tax incentives for insurers could catalyse the development of the insurance industry.

- Flexible hydrogen contracts with variable offtake agreements can a) empower electrolyser operators to pursue dynamic business models that optimise hydrogen and renewable power sales or b) monetise excess production. Many hydrogen offtakers currently lack the operational flexibility to ramp production but advancements in hydrogen storage or technologies in key offtake sectors could address this gap.

- Power guarantees from the renewable developer to provide a minimum quantity of hourly EACs could provide more predictability. However, guarantees may be challenging to negotiate and could increase supply contract costs. The development of secondary power or EAC markets could help optimise the distribution of risk.

Risk 2: Logistic complexity

The challenge

Green hydrogen developers face significant project design and execution complexities, as they navigate construction and operation of renewable power and electrolysis assets. The current 36-months vintage component requires near simultaneous construction of assets, while the hourly matching requirement necessitates closely coordinated operation. This means that both the renewables project and the hydrogen project are dependent on the success of another project that is itself uncertain.

Developers who opt to build behind-the-meter renewables to meet this requirement face a double-sided challenge often referred to as “project on project risk.” In this archetype, hydrogen production is contingent upon the timely completion and operation of the associated renewable project. Likewise, the renewables project is dependent on the timely completion of the hydrogen project for revenue. If either project experiences delays, the profitability of the other will be at risk. The nascency of the industry creates a high risk that hydrogen projects will not be built on time or will be smaller than originally planned.

Developers who opt for vPPAs or PPAs face a similar challenge, though the risk is spread between the hydrogen and renewables developers. The renewable energy supplier’s financing could face hurdles if the hydrogen project is the sole offtaker. In regions with high-performing renewables, there will also likely be intense competition for resources from other high willingness-to-pay industries. Renewables developers may favour these alternative buyers because hydrogen projects are seen as a risky source of revenue.

In addition to the challenge of simultaneous asset construction, vPPA and PPA configurations must also coordinate simultaneously with the asset operations of the power producer and the offtaker. Electrolyser operators need to juggle multiple data feeds, integrating fluctuating real-time price reports, weather conditions forecasts, and real-time operations data from their renewable energy assets so they can quickly ramp production down if renewables stop producing. Errors in this data could lead to a substantial tax credit loss if renewables stop producing due to forecasting errors or technical malfunctions but the electrolyser continues to consume electricity.

Potential solutions

To mitigate project on project risk:

- BTM developers could adopt a phased approach, first constructing renewables and integrating hydrogen production integrated later. This would likely require the developer to find another offtaker for their renewable power to provide revenue before the hydrogen project comes online.

- PPA and vPPA developers can explore novel power contracting approaches, such as partnering with existing large buyers, like technology companies, as a paired offtaker. This approach can help mitigate risk for renewable developers by avoiding the uncertainties associated with aligning their projects with an emerging industry like hydrogen.

- Cross-collateralisation of a portfolio of smaller first-mover projects could reduce the likelihood that isolated errors in any single project will substantially disrupt cashflows to project owners.

Emerging data management solutions to streamline simultaneous operation risk are already being explored by power market service providers.

Risk 3: Grid volatility & uncertainty

The challenge

Hydrogen project developers with grid-connected projects (vPPA, PPA, or hybrid) can face uncertainty from the short-term, minute-to-minute, hour-to-hour, and month-to-month volatility of the electricity market as well as from the rapidly evolving long-term, year-over-year electricity price environment. To protect against the different temporal dimensions of market volatility, developers can secure physical PPAs or vPPAs, (or opt for behind-the-meter systems, which are largely insulated from all the risks described in this section), but there are trade-offs for either option.

Physical PPAs limit the risk of short-term volatility by delivering power at a pre-determined cost with exposure to wholesale price uncertainty only in the sale of excess contracted power back to the grid. However, in the long term, developers risk their projects becoming uncompetitive if PPA prices significantly decline over time.

vPPA configurations experience greater risk from short-term varying power costs because they are exposed to the wholesale market via the contract for differences settlement (CfD) and to the commercial rates via their physical power purchases from the utility. The CfD settlement, which will provide additional revenue to the hydrogen project when prices are high, creates a hedge against long-term increases in the commercial market price, as long as the wholesale price is driven up by the same factors. However, changes in the grid’s energy sources over time can weaken the correlation between the CfD and the commercial prices creating the potential for hedging strategy failures. The first figure above demonstrates the uncertainty in future price evolution reported by ERCOT itself. The second figure above shows the potential consequences of failing to manage wholesale price volatility. A single month in which the average cost of power is more than $160/MWh, as shown in August of 2023, could do irreparable damage to project economics.

Additionally, grid-connected projects may face significant delays due to interconnection queues, as they depend on timely grid access to start production with EACs. Curtailment risks can further complicate hydrogen production, as solar or wind farms can be forced to scale back operations when grid capacity is exceeded, leaving excess energy unused and potentially missing hours of matching EAC.

Potential solutions

To mitigate grid-related risks, the following market and policy solutions exist:

- Build onsite renewable or contract with projects physically close to reduce grid exposure and the risks of curtailment at different nodes within the grid. This can be for part or all the electrolyser capacity but may increase weather variability risk.

- Enter contracts with retail energy providers to fix electricity consumption costs. These are likely only widely available in deregulated markets and are subject to term negotiation. They could reduce costs vs traditional retail rates if the developer is able secure value for being a flexible load.

- Collaborate with Regional Transmission Organisations and federal or state policymakers to streamline grid interconnection processes and identify areas in the system that would benefit from both additional capacity and a large flexible load like a hydrogen plant.

- Support development of spot hourly EACs to provide an additional, more liquid source of hourly EACs to enable production during times of supply-driven curtailment.

Next steps

As tax credit uncertainty increases, developers and offtakers alike must proactively address the risks that will persist regardless of regulatory outcomes. Challenges such as weather variability, logistics complexity, and the future of the grid will endure even after final rules are in place. Many market-driven solutions exist, but these investments are costly, high risk, and have long lead times that may necessitate additional government support. Stakeholders can begin collaborating to identify and mitigate these risks, accelerating project deployment once the guidance is released.